Your Zestimate Is Not Market Analysis

If you are thinking about selling your home, there is a good chance you have already looked it up online.

Most sellers have.

There is nothing wrong with curiosity. The problem starts when that number begins doing real work in your head. When you build your expectations around it. When you decide whether to sell, what to ask, or whether to take an offer based on what an algorithm says your home is worth.

Here is what you need to understand:

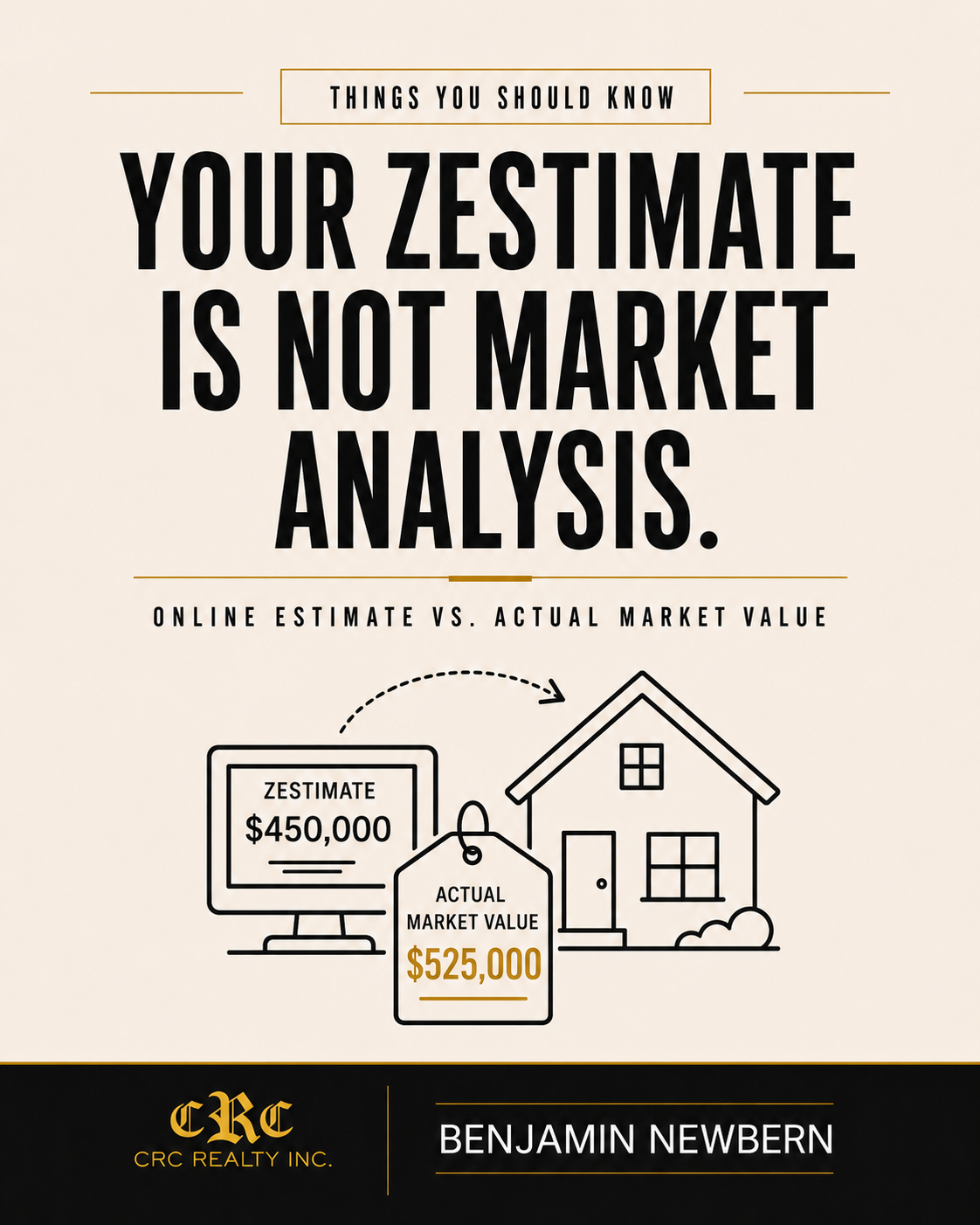

Your Zestimate is not market analysis.

What Automated Estimates Actually Are

Zillow’s Zestimate — and similar tools from Redfin, Realtor.com and other sites — are automated home-value estimates. They use available data, property records, sales history, market trends and statistical models to estimate a property’s value.

That can be useful as a starting point.

But it is not the same thing as a local pricing analysis.

An automated estimate does not walk through your house. It does not know whether you renovated the kitchen. It does not know whether the roof is two years old. It does not know whether the previous owner deferred maintenance for a decade. It does not know whether your street consistently sells higher than the next one over because of lot sizes, traffic patterns or buyer preference.

It is working from data.

A good market analysis is built from data plus judgment.

The Shoals Is a Local Market

This matters more here than it might in a major metro with thousands of transactions smoothing out the numbers.

The Shoals is a smaller, more localized market. Individual sales can move comps. One strong sale on your street can matter. So can one distressed sale. A gut renovation nearby affects value differently than a cosmetic flip two neighborhoods over.

The gap between what an automated estimate says and what a buyer will actually pay — based on what their agent sees in SAAR MLS — can be substantial.

I have run CMAs where the Zestimate was $30,000 high. I have run others where it was $25,000 low.

Neither situation helps you.

Overpricing costs you days on market, negotiating leverage and, often, money. Underpricing means you risk leaving equity on the table at closing.

What a CMA Actually Does

A Comparative Market Analysis starts with verified closed sales.

Not list prices.

Not online estimates.

Not what someone hoped to get.

Closed sales.

Those sales are pulled from SAAR MLS and filtered for properties that are genuinely comparable to yours in size, condition, age, location and timing.

From there, a good agent builds a pricing range that accounts for how your home compares to what actually sold: where it is stronger, where it is weaker and what the active competition looks like right now.

That is the kind of analysis a buyer’s agent may review before advising a client on what to offer.

It is also the kind of pricing logic that has a better chance of holding up during appraisal.

Before You Price Your Home, Get a Real Number

You do not have to be ready to list to ask for a CMA.

A lot of sellers get one months before they plan to move just to understand where they stand. It costs nothing, it carries no obligation and it gives you something an online estimate cannot: an honest, data-driven picture of what your home may be worth in today’s Shoals market.

If you would like one, reach out. I am happy to run it.

Benjamin Newbern is a licensed REALTOR® with CRC Realty in Florence, Alabama, serving buyers and sellers throughout the Shoals. AL License #000169445.